Tax Implications of Home Renovation: What You Can and Can’t Deduct

DECEMBER 01, 2025

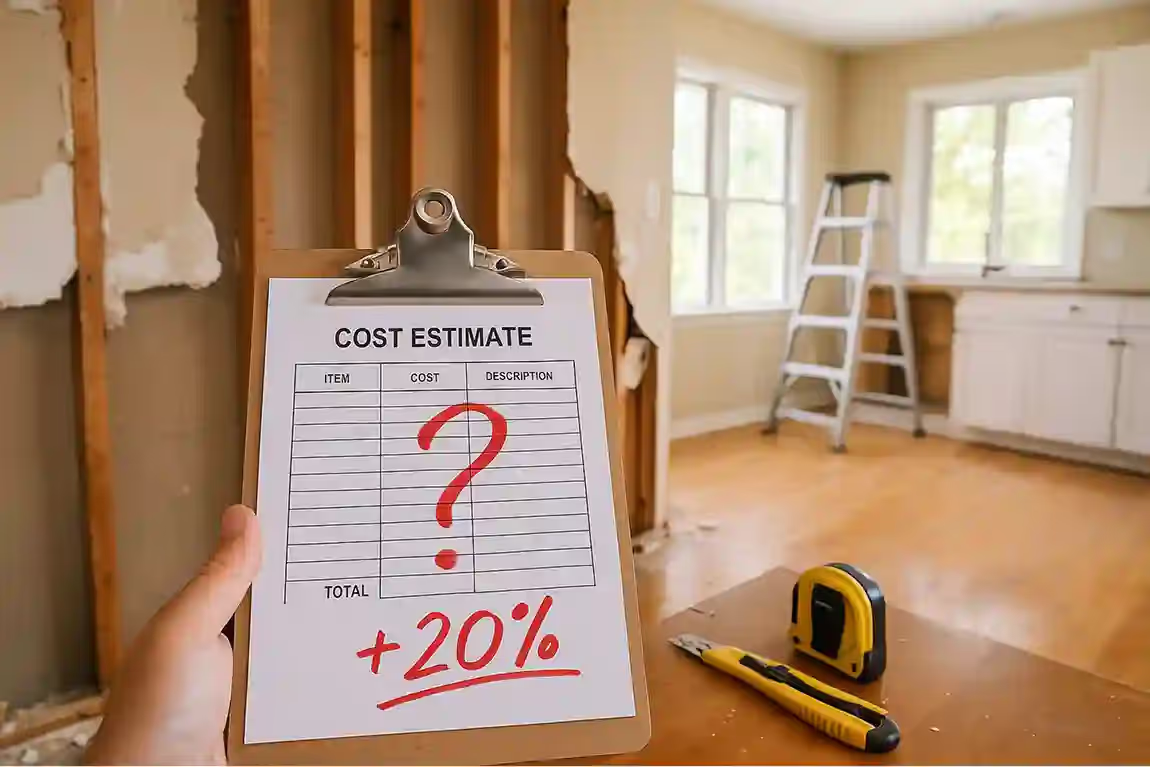

A homeowner demolishes a bathroom wall, discovering black mold spreading through the framing and into the subfloor—a $15,000 problem that didn't exist in the original $12,000 renovation plan. Another family orders imported Italian tile, only to learn mid-project that shipping costs have tripled due to supply chain disruptions, adding $8,000 to their kitchen backsplash alone. A third renovator watches in horror as their contractor uncovers termite damage behind what was supposed to be a simple cabinet replacement, turning a weekend project into a two-month structural repair costing $25,000. These aren't horror stories from a reality TV show—they're the everyday reality of home renovations where emergency funds don't exist. The 20% contingency rule isn't just financial wisdom; it's the difference between a successful transformation and a nightmare that haunts your finances for years.

When homeowners dream about renovations, they envision pristine new spaces, enhanced functionality, and increased property value. The excitement of selecting materials, approving designs, and watching progress unfold creates an optimistic bubble where problems seem distant and manageable. This psychological optimism leads to precise budgeting that accounts for every known expense while completely ignoring the unknown disasters lurking behind walls and beneath floors. According to research from Clever Real Estate, approximately 78% of remodeling projects exceed their initial budget, with 44% exceeding their budget by at least $5,000 and 35% surpassing their budgets by $10,000 or more. The 20% contingency rule exists specifically to address this reality gap between careful planning and chaotic execution, providing homeowners with a financial buffer that prevents mid-project crises from derailing their dreams and turning exciting improvements into sources of lasting financial stress and regret.

Understanding why emergency funds prove essential requires shifting your mindset from idealistic planning to realistic preparation. Unlike purchasing a new car or appliance where price is fixed and known, remodeling involves opening up your home's hidden infrastructure, revealing problems that couldn't be diagnosed during initial inspections. The contingency fund isn't a luxury or an admission of poor planning—it's a recognition that houses are complex systems where each layer conceals potential complications. Financial advisors and remodeling professionals universally recommend setting aside 10% to 20% of your total project budget as emergency money, yet fewer than 30% of homeowners actually follow this guidance, creating a predictable pattern of mid-project financial crisis and compromised outcomes. The Houzz Home Study reveals that among homeowners who set a budget, nearly 40% exceeded it, compared to 34% who went over budget two years prior—demonstrating that budget overruns are becoming more common, not less, as renovation complexity and material costs continue to rise in today's volatile economic environment.

The 20% contingency rule represents a risk management principle that allocates a specific percentage of your total renovation budget to unforeseen expenses that emerge during construction. This isn't a random number—it's derived from decades of industry data analyzing thousands of remodeling projects across different home ages, project scopes, and geographic regions. The percentage acknowledges that even with meticulous planning, professional inspections, and experienced contractors, hidden issues will surface once walls open up and old systems get exposed to modern inspection standards. The Joint Center for Housing Studies at Harvard University has tracked remodeling trends for over three decades, and their research consistently shows that homes built before 1980 require significantly more contingency than newer construction due to outdated building codes, materials that have degraded over time, and systems that no longer meet modern safety standards. Americans spent over $600 billion on home improvements and repairs in recent years, and a substantial portion of that spending came from unexpected discoveries rather than planned upgrades, highlighting how universal and unavoidable these surprise expenses have become.

The recommendation ranges from 10% to 20% depending on project risk factors. A straightforward cosmetic update in a newer home might require only 10% contingency, while a major gut renovation in a century-old house demands the full 20% buffer. Risk factors that push you toward the higher end include homes built before 1980 when building codes were less stringent, projects involving plumbing or electrical system updates, renovations that require structural modifications, properties with previous DIY work or unpermitted additions, and any project where the full scope cannot be determined until demolition reveals existing conditions. The National Association of Home Builders (NAHB) represents nearly 50,000 members involved in the remodeling industry, and their professionals consistently advise that contingency planning separates successful projects from financial disasters. When you're dealing with homes that have been modified by multiple owners over decades, each layer of renovation conceals potential problems that only emerge when contractors begin their work, making the contingency fund an essential tool for navigating uncertainty rather than an optional expense that budget-conscious homeowners can safely eliminate.

Think of contingency money as insurance rather than extra spending money. Just as you wouldn't drive without auto insurance despite being a careful driver, you shouldn't renovate without financial protection against the unpredictable. The 20% rule ensures that when your contractor discovers rotted floor joists beneath your planned new bathroom tile, you have immediate funds available to address the problem properly rather than resorting to dangerous shortcuts or halting the project while you scramble for financing. Resources from the Consumer Financial Protection Bureau emphasize that emergency funds provide the psychological security needed to make sound decisions under pressure rather than panic-driven choices that create long-term problems. Their research demonstrates that consumers with emergency savings are significantly less likely to experience delinquent debt or financial hardship when unexpected expenses arise, making contingency funds not just practically important but psychologically essential for maintaining clear-headed decision-making during stressful renovation situations where every choice affects both immediate outcomes and long-term home value.

Humans possess a remarkable ability to visualize positive outcomes while simultaneously minimizing potential negative scenarios—a cognitive bias that serves us well in many life areas but proves catastrophic in renovation planning. This optimism bias leads homeowners to believe their project will be the exception to statistics, that their careful planning and good intentions will prevent the problems that plague other renovators. They examine their budget line by line, convinced that each item is accurate and complete, never considering that the most expensive items are the ones they cannot yet see. The planning fallacy, a well-documented psychological phenomenon studied extensively by behavioral economists, causes people to systematically underestimate the time and cost required to complete future tasks. In remodeling, this manifests as homeowners focusing on visible surface elements while completely ignoring what lies beneath—budgeting meticulously for the perfect subway tile, the quartz countertops, the custom cabinetry, while never considering that their 1960s electrical system cannot support modern appliance loads or that water damage from a slow leak has compromised the subfloor beneath where that beautiful tile will sit. This cognitive blind spot affects even experienced homeowners who have completed previous renovations, because each project presents unique hidden conditions that cannot be predicted from past experience.

Financial pressure also drives the decision to skip contingency funds, particularly when homeowners are already stretching their maximum budget to achieve their dream renovation. The $50,000 kitchen remodel feels just barely possible, and adding a $10,000 contingency transforms it into an impossible $60,000 project—so they convince themselves the contingency isn't necessary. This dangerous math ignores the fact that discovering a major problem without contingency funds will either kill the project entirely or force financing at unfavorable terms, ultimately costing far more than the original 20% buffer would have. According to the 2024 Houzz Home Study data from Family Handyman, the percentage of homeowners spending more than $25,000 on their renovation rose to 51% in 2023, up from 37% in 2020, indicating that renovation ambitions are growing faster than realistic budget planning. Many of these high-spending homeowners enter projects without adequate contingency, setting themselves up for financial strain when inevitable surprises emerge and forcing difficult choices between project quality, timeline, and personal financial stability.

Contractor bidding processes often reinforce this optimism in ways that disadvantage homeowners. While reputable contractors mention the need for contingency funds, homeowners focused on the bottom line treat this advice as optional upselling rather than essential risk management. Competitive bidding encourages contractors to provide lean estimates that minimize contingency to win jobs, creating a race to the bottom where realistic budgeting gets punished and unrealistic optimism gets rewarded—until reality strikes midway through demolition. Some contractors intentionally lowball initial bids knowing they'll recover the difference through change orders when problems inevitably surface, a practice that preys on homeowner optimism and creates adversarial relationships mid-project. The ethical contractors who provide realistic estimates including contingency recommendations often lose bids to competitors who tell homeowners what they want to hear rather than what they need to know. This dynamic perpetuates the cycle of budget overruns and reinforces the false belief that contingency planning is optional rather than essential, leaving homeowners vulnerable to financial surprises they could have anticipated with proper professional guidance.

Structural surprises represent the most expensive category of unexpected renovation costs, often discovered during demolition when contractors remove drywall to find rotted framing, termite damage, or foundation issues that compromise the entire project's integrity. A simple kitchen cabinet removal might reveal that a previous homeowner removed a load-bearing wall without proper support, requiring $10,000 in engineered beams and permits before new cabinets can even be considered. Bathroom tile demolition could expose decades of water damage that extends into adjacent rooms, turning a $15,000 remodel into a $35,000 reconstruction. According to the EPA's guide to mold and moisture, mold may be hidden in places such as the back side of drywall, wallpaper, or paneling, the top side of ceiling tiles, and the underside of carpets and pads—locations that remain invisible until renovation work begins. These structural realities cannot be diagnosed during initial consultations because they hide behind finished surfaces, making contingency funds the only defense against financial devastation when such problems emerge unexpectedly and demand immediate resolution before any cosmetic work can proceed.

System failures emerge when older electrical, plumbing, or HVAC systems cannot support modern demands or fail inspection when exposed to current code scrutiny. Your 1970s electrical panel might have functioned adequately for basic lighting and appliances, but adding a chef-grade range, quartz countertop outlets, and under-cabinet lighting could push it beyond safe capacity, requiring a $3,000 panel upgrade. Cast iron drain pipes that seemed fine during initial assessment might crumble when disturbed, demanding complete replacement that adds $5,000 to your bathroom renovation. Building codes change over time, and your renovation project may reveal that your plumbing and electrical systems are so old that they are no longer up to code—a discovery that transforms optional upgrades into mandatory corrections. The RenoFi analysis of renovation budgets confirms that kitchens and bathrooms are the rooms most commonly going over budget, largely because they involve complex systems hidden behind walls—exactly the type of surprise your contingency fund exists to address. Old plumbing from before the 1960s generally used galvanized pipes prone to corrosion, clogging, and leaking, while outdated electrical wiring can pose dangerous fire risks that inspectors will require you to address before approving your renovation work. These system discoveries aren't optional upgrades—they're mandatory safety corrections that must be completed before the project can proceed legally or safely.

Material cost volatility has become increasingly unpredictable due to supply chain disruptions, trade policies, and global demand fluctuations. That quote for imported tile valid for 30 days might increase 25% when you finally order three months into the project. Lumber prices that seemed stable during planning could spike due to wildfire impacts or tariff changes, adding thousands to framing costs. Even domestic materials face availability issues where a manufacturer's backorder forces you to choose between project delays or substituting a more expensive alternative. The Bureau of Labor Statistics data on construction materials shows that material costs increased dramatically during the pandemic period and have remained elevated, with price volatility creating budgeting challenges that didn't exist in more stable economic periods. According to the Home Builders Institute, an estimated 2.2 million construction workers will need to be hired and fully trained within the next three years to meet projected home renovation demand, indicating that labor shortages may continue to create scheduling challenges and cost pressures for the foreseeable future. Contingency funds provide the flexibility to absorb these price shocks without sacrificing design quality or timeline, allowing homeowners to proceed with confidence even when market conditions shift unexpectedly.

Labor complications create unexpected expenses when specialized subcontractors discover complications that require additional time or expertise. A tile installer might find that your subfloor is too uneven for large-format tiles, requiring a $1,500 leveling system before installation can begin. An electrician could discover that your walls contain asbestos-containing wiring insulation, triggering abatement procedures that add $2,000 and a week of delays. These aren't contractor errors or attempts to upsell—they're legitimate challenges that experienced professionals couldn't anticipate during initial walkthroughs but must address to deliver quality, code-compliant work that protects your family and your investment. The intersection of aging housing stock, increasingly stringent building codes, and rising material costs creates a perfect storm of renovation budget risk that only adequate contingency planning can address, transforming potential disasters into manageable challenges that skilled contractors can resolve without derailing the entire project or forcing homeowners into debt-financed emergency responses.

Discovering a major problem without contingency funds creates a cascade of financial consequences that extend far beyond the immediate repair cost. Homeowners typically face three terrible options, each with lasting negative impacts. First, they can halt the project entirely, living in a construction zone for months while saving additional money, during which time exposed plumbing might corrode, materials could get damaged, and contractor schedules may become unavailable, compounding delays and costs. This pause often leads to project abandonment, where homeowners accept a half-finished disaster rather than finding the additional funds. The Clever Real Estate research found that 32% of homeowners have stopped a renovation midway through because of unexpected costs—a statistic that represents countless families living in incomplete spaces, their investments providing no return, their homes less functional than before the project began, and their daily lives disrupted by the constant reminder of a failed project they cannot afford to complete.

Second, they can finance the emergency expenses through high-interest credit cards or personal loans, turning a $5,000 problem into a $7,500 expense after interest payments. Many homeowners tap available credit lines without calculating the true cost over repayment periods, and the stress of accumulating debt transforms what should be an exciting improvement into a source of anxiety and marital conflict. The same Clever Real Estate study found that 63% of homeowners have taken on debt to pay for renovation completion, with 33% borrowing $10,000 or more for their most recent project. Alarmingly, 36% of these homeowners struggled to pay off their credit card bills after their renovation was complete, indicating that debt-financed renovations create lasting financial strain that persists long after the sawdust settles. The financial burden extends years beyond project completion, overshadowing any enjoyment of the renovated space and creating stress that affects every aspect of daily life, from career decisions to family relationships to retirement planning.

Third, they can pressure contractors to implement cheap, inadequate fixes that meet immediate budget constraints but fail within months or years, requiring expensive corrections that exceed what proper initial repairs would have cost. This approach also creates liability issues; improper repairs discovered during home sales can trigger legal disputes and required remediation that sellers must finance under pressure. A foundation crack patched with cheap epoxy rather than properly stabilized might pass initial inspection but cause extensive damage during the next heavy rain. Electrical work done without permits to save money becomes a nightmare when selling, potentially requiring walls to be opened and all work redone to meet code. The short-term savings become long-term financial disasters that compound the original problem exponentially, often costing three to five times what proper initial repairs would have required while creating safety hazards that put families at risk during the intervening years.

The psychological cost of unpreparedness often exceeds the financial damage. Living in a half-finished space creates daily stress that affects work performance, relationships, and mental health. Homeowners report feelings of failure, resentment toward contractors (who often aren't at fault), and regret that taints the entire renovation experience. The CFPB research on financial well-being demonstrates that consumers without emergency savings experience significantly higher levels of financial stress and lower financial well-being scores. This emotional toll doesn't appear in budget spreadsheets but represents a significant life impact that proper contingency planning could have prevented. The stress of budget overruns affects nearly 80% of renovating homeowners, creating health impacts that persist long after projects complete and fundamentally changing how families experience their homes—transforming spaces meant to bring joy into constant reminders of financial difficulty and compromised dreams.

Managing contingency funds requires separating this money from your primary renovation account to prevent accidental spending on planned items. Create a dedicated savings account or line of credit specifically labeled "Renovation Emergency Fund" that requires separate authorization to access. This psychological barrier prevents the common scenario where homeowners gradually dip into contingency for "just this one upgrade," then discover there's no money left when real emergencies emerge. The fund should remain untouched until a genuine unforeseen problem requiring immediate attention appears. Many financial institutions offer high-yield savings accounts that can hold your contingency funds while earning modest interest during the months your project is underway—a small benefit that adds up during longer renovations. The University of South Alabama analysis of renovation statistics shows that although nearly a quarter of homeowners had no renovation budget in 2023, 76% set one initially—and of those who set a budget, nearly 40% exceeded it. This demonstrates that even homeowners who plan carefully face overruns, making contingency funds essential regardless of how thorough your initial planning appears.

Access protocols should require contractor documentation, photographic evidence of the problem, and homeowner approval before releasing funds. This prevents contractors from viewing contingency as a slush fund for minor changes or upgrades they prefer. Establish clear criteria: contingency covers hidden conditions that couldn't be reasonably discovered during initial inspection, code compliance issues that emerge when walls open up, structural problems that affect safety, and material cost increases beyond your control. It should not cover change orders where you decide to upgrade finishes, add features, or modify the original scope—these require separate funding and decision-making. Communication protocols with your contractor should establish that contingency funds exist but are not automatically available. When a potential issue arises, the contractor should provide a written explanation with photos, a detailed cost estimate for the fix, and alternative solutions if available. This documentation creates accountability and ensures you're making informed decisions rather than panic-driven approvals that you might regret once the immediate pressure subsides.

Phase-based allocation distributes your contingency across project stages according to risk level. During demolition and structural work—when you're most likely to discover major problems—reserve 40% of your contingency. Allocate 30% to electrical and plumbing rough-in, another period where hidden issues commonly surface. Save 20% for finish work where material price changes or minor adjustments might be needed, and keep 10% as a final buffer for post-completion touch-ups. This phased approach prevents spending contingency too early on minor issues, leaving insufficient funds for major discoveries later in the project. The discipline of phase-based allocation forces homeowners to evaluate each potential contingency expenditure against remaining project risk, ensuring that funds remain available when they're most needed rather than being depleted by early, less critical discoveries that could potentially be addressed through alternative solutions or deferred until after the main project completes.

"My contractor said we don't need contingency because they're experienced and have done many similar projects." This red flag statement indicates either contractor inexperience or dishonesty. Even the most seasoned professionals cannot see through walls or predict material cost fluctuations. Experienced contractors actually insist on contingency because they've learned through hard experience that unexpected issues are normal, not exceptional. A contractor who minimizes contingency concerns is likely planning to issue change orders when problems emerge, or they're cutting corners by ignoring code requirements and safety issues they'd otherwise need to address. The best contractors are transparent about uncertainty and help homeowners prepare for it rather than pretending it doesn't exist, because they understand that realistic expectations at the project's start create better client relationships and smoother execution than optimistic promises that inevitably collide with renovation reality.

"We can't afford to set aside money we might not need—we're already at our maximum budget." This argument confuses the contingency fund as optional when it's actually essential. If you cannot afford the project plus 20% contingency, you cannot afford the project. Reducing scope to create room for emergency funds always proves wiser than proceeding without a safety net. A smaller, well-executed renovation that stays within a protected budget provides more satisfaction than an ambitious project that becomes a financial disaster when the inevitable problems appear. Consider phasing your renovation into smaller projects over time rather than attempting everything at once without adequate financial protection. The NAHB Remodeling Market resources provide valuable data on remodeling spending trends that can help you understand whether current market conditions favor aggressive or conservative budgeting in your area, allowing you to make informed decisions about project timing and scope that account for both your financial capacity and market realities.

"We've already had a home inspection, so we know the condition of everything." Standard home inspections provide surface-level assessments but cannot evaluate what's hidden within walls, under floors, or above ceilings. Inspectors specifically limit their liability by stating they cannot see inside structures or predict future failures. They're looking for obvious defects, not performing exploratory surgery on your home. Many catastrophic discoveries occur in homes that passed inspections with flying colors because the issues were concealed and systems were functioning adequately (but not safely) before renovation exposed them to modern standards. A pre-purchase inspection examines visible conditions at a point in time; a renovation project opens walls and disturbs systems in ways that reveal problems no inspection could have identified without demolition. The false confidence created by clean inspection reports leads homeowners to skip contingency planning precisely when they need it most—in older homes where hidden conditions are most likely to create expensive surprises.

"We'll just use credit cards if something comes up." This approach ignores the true cost of high-interest financing and the psychological impact of debt-fueled renovation stress. Credit card interest rates often exceed 20% APR, turning a $5,000 emergency into a $6,500 expense over typical repayment periods. More importantly, the lack of dedicated funds forces panic-driven decisions where homeowners choose the cheapest fix rather than the right fix, creating long-term problems that compound the initial issue. The financial planning principles that govern emergency funds in general life apply doubly to renovations, where surprise expenses are more rule than exception. Having dedicated contingency funds allows you to evaluate options calmly, choose quality solutions, and maintain the integrity of your renovation rather than compromising under financial pressure that forces suboptimal choices with lasting consequences for both home value and daily livability.

"We've included a 5% buffer, which should be plenty." Five percent contingency might adequately cover minor finish changes or small price fluctuations, but it disappears instantly when a single structural issue emerges. Most experts recommend 10% as the absolute minimum for very low-risk projects in newer homes, with 15-20% being appropriate for typical renovations. The difference between 5% and 20% on a $50,000 project is $7,500—the exact cost of many common discoveries like electrical panel upgrades or water damage repair. Underestimating contingency needs represents one of the most expensive budgeting mistakes homeowners make, and the consequences extend far beyond the immediate financial impact to affect project quality, timeline, and homeowner satisfaction for years to come. The false economy of inadequate contingency creates far more problems than it solves, trading modest upfront savings for potentially massive mid-project crises that disrupt lives and drain finances.

Start with a comprehensive project scope that details every element of the renovation, from demolition through final cleanup. Include line items for permits, design fees, material delivery charges, dumpster rentals, and post-construction cleaning—these "invisible" costs often total 10-15% of the project but rarely appear in initial estimates. Research actual material costs by visiting suppliers and getting current quotes, not relying on outdated online estimates or contractor allowances that may be unrealistic. For labor costs, obtain at least three detailed bids from licensed contractors, ensuring each includes identical scope so you're comparing real numbers, not assumptions. The National Association of the Remodeling Industry (NARI) provides resources for finding qualified contractors and understanding realistic project costs in your area, helping homeowners establish budgets grounded in current market conditions rather than wishful thinking or outdated information.

Once you have a realistic base budget, add your contingency percentage based on project risk assessment. Add another 5-10% for "project creep"—the inevitable upgrades and improvements you'll want to make once you're already invested. This might include upgrading from standard to soft-close cabinet hinges, adding that accent tile you fell in love with, or choosing a better appliance package once you're already spending significant money. These aren't emergencies but they are realities, and budgeting for them prevents stress and disappointment. Include a separate category for temporary living expenses if the renovation will displace you from kitchens, bathrooms, or bedrooms. Extended hotel stays or short-term rentals often become necessary for major projects, costing $2,000-$5,000 that homeowners forget to budget. Factor in increased food costs from takeout during kitchen renovations, plus potential pet boarding or child care during construction phases. These indirect costs significantly impact total project expense but rarely appear on contractor quotes, creating budget surprises that deplete contingency funds meant for actual construction emergencies.

The final budget calculation follows this formula:

Base Renovation Costs + Contingency (15-20%) + Project Creep Buffer (5-10%) + Temporary Living Expenses + Design/Permit Fees = True Project Cost. Only when this complete calculation fits your financial capacity should you proceed. The 60/20/20 rule some professionals recommend—60% materials and finishes, 20% skilled labor, 20% contingency—provides a simplified framework, but your specific project may require adjustments based on complexity and risk factors. For complex projects, consider consulting with a fee-only financial advisor who can help you evaluate how renovation financing fits into your broader financial picture, including retirement savings, emergency reserves, and other financial goals that home improvement decisions affect. The investment in professional financial guidance often pays for itself many times over by preventing costly mistakes and ensuring that renovation ambitions align with overall financial health and long-term security.

Establishing clear criteria for accessing contingency funds prevents premature spending while ensuring legitimate emergencies get addressed properly. Your decision matrix should evaluate each unexpected expense against four factors: safety implications, code compliance requirements, project completion necessity, and long-term cost avoidance. Safety issues affecting structural integrity, electrical hazards, or gas lines automatically qualify for immediate contingency use—there's no negotiation when lives are at risk. These problems must be fixed correctly, and your emergency fund exists precisely for this purpose. Never allow budget concerns to compromise safety, as the consequences of inadequate repairs can include injury, death, or liability that far exceeds any renovation budget. The American Society of Home Inspectors provides standards and resources that can help homeowners understand the difference between cosmetic issues and safety hazards that demand immediate attention regardless of budget impact.

Code compliance discoveries that emerge when walls open up represent another automatic contingency use. If your city inspector demands code upgrades for any system you're touching, you must comply or face stop-work orders, fines, and potential problems when selling. This isn't optional work—it's legally mandated. While it feels unfair to spend money upgrading electrical outlets you hadn't planned to replace, the alternative is failed inspections, project delays, and potentially ripping out finished work to access the systems later. Building codes exist to protect occupants, and renovation projects that expose non-compliant systems create legal obligations that homeowners cannot ignore regardless of their budget preferences. The short-term frustration of unexpected code compliance expenses pales compared to the long-term consequences of ignoring legal requirements that affect home safety, insurability, and resale value.

Project completion necessity means evaluating whether the problem prevents you from completing the original scope. A minor crack in an otherwise sound wall might be cosmetic and can wait, but a structural issue that prevents installing new cabinets must be addressed. This category requires judgment calls. Ask: "Can we safely complete the renovation as planned without fixing this?" If the answer is no, contingency funds should cover it. If the answer is yes but it's imperfect, you might negotiate with your contractor to document the issue and address it later when funds are available. Long-term cost avoidance evaluates whether spending contingency now prevents exponential future expenses. Discovering minor termite damage might cost $1,000 to treat today, but waiting could result in $10,000 in structural repairs five years later. Similarly, upgrading an undersized electrical panel during kitchen renovation costs $3,000, while doing it later as a standalone project might cost $5,000 due to access issues and minimum service call charges. These preventive uses of contingency represent wise investments rather than emergencies, but they should still be documented and justified before approval to maintain the discipline that protects remaining funds for genuine surprises.

Sarah and Michael planned a $45,000 kitchen renovation in their 1950s ranch home. Despite their contractor recommending a 15% contingency, they insisted they couldn't afford more than $47,000 total. When demolition revealed extensive termite damage in the wall behind the sink, the required treatment and framing replacement added $6,800. Without contingency, they put the charges on a credit card at 24% APR, increasing their total project cost to $53,800 plus $1,500 in interest over the two years it took to pay off. The financial strain caused arguments and delayed other planned improvements. Sarah later admitted, "We spent more than if we'd just listened and planned properly. The stress wasn't worth the false sense of saving money upfront." Their experience illustrates how avoiding contingency planning doesn't actually save money—it simply shifts costs to higher-interest financing while adding stress that affects quality of life and relationships, turning what should have been an exciting home improvement into a source of lasting regret and financial burden.

Conversely, James budgeted $60,000 for his bathroom renovation with a proper 20% contingency of $12,000. During demolition, his contractor discovered the cast iron drain pipe had completely rusted through, requiring $4,500 in emergency plumbing work. Because James had contingency funds available, the work proceeded without delays or stress. He still had $7,500 remaining when a supply chain issue doubled the cost of his selected tile, allowing him to either upgrade to a different material or absorb the increase without compromise. His total project cost $66,500—just 10% over his base budget—and completed on schedule. James reflects, "Having that cushion let us make smart decisions instead of desperate ones. It was the smartest part of our entire renovation." His experience demonstrates how contingency funds don't just provide financial protection—they enable better decision-making that improves outcomes throughout the project, preserving both the homeowner's vision and their peace of mind.

The Rodriguez family planned a $100,000 whole-house renovation and set aside 18% contingency based on their contractor's risk assessment. During structural work, they discovered the previous owner had removed a load-bearing wall and installed an inadequate beam, causing sagging floors throughout the main level. The engineered solution cost $22,000—more than their $18,000 contingency. However, because they'd planned responsibly, they could finance only the $4,000 shortfall rather than the full amount, making the emergency manageable. Their contractor noted that without any contingency, the project would have halted for months while they secured additional financing, potentially causing weather damage to the opened structure and doubling the effective cost. Their experience shows that even when contingency proves insufficient, having substantial reserves dramatically improves outcomes compared to having none at all, demonstrating why the 20% rule represents a minimum guideline rather than a guaranteed ceiling on unexpected expenses.

Linda's experience demonstrates the danger of insufficient contingency. She budgeted $25,000 for a kitchen refresh with only 5% contingency ($1,250), believing her 1990s home was too new for major surprises. When the backsplash demolition revealed extensive mold from a slow plumbing leak, remediation alone cost $3,800. Without adequate funds, Linda chose the cheapest remediation option that didn't address the underlying moisture source, only to have mold return within six months, requiring another $5,000 in proper remediation plus cabinet replacement. Her attempt to save $3,750 in contingency ultimately cost an additional $8,800 and months of health concerns and frustration. Her story illustrates how inadequate contingency doesn't just delay proper solutions—it often forces homeowners toward cheap fixes that create larger problems requiring more expensive corrections later, transforming modest initial savings into massive long-term costs while exposing families to health hazards that could have been properly addressed from the start.

The 20% contingency rule isn't a suggestion from overcautious professionals—it's a data-driven necessity based on the lived experience of millions of homeowners who've navigated the chaotic reality of renovation. Just as you wouldn't drive without insurance because "you're a careful driver," you shouldn't renovate without emergency funds because "you've planned carefully." The unexpected is the only guarantee in remodeling, and financial preparation is the only protection against the discoveries that await behind every wall and beneath every floor. The statistics are clear: 78% of homeowners exceed their budgets, 87% face challenges during renovation, and 74% report regrets after completion—numbers that would be dramatically different if more homeowners embraced rather than avoided contingency planning. The National Association of Realtors remodeling research consistently demonstrates that well-planned renovations deliver both financial returns and personal satisfaction, while poorly planned projects create lasting regret regardless of the quality of the finished work.

Your contingency fund buys more than financial protection—it purchases peace of mind, decision-making clarity, and the ability to handle crises without derailing your entire life. It prevents the marital stress of mid-project financial panic, the health impacts of living in perpetual construction, and the long-term regret of compromised outcomes. The homeowners who survive renovation with their sanity and finances intact are universally those who respected the 20% rule and treated contingency as essential rather than optional. They report higher satisfaction with their completed projects, less financial stress during and after renovation, and greater confidence in their ability to maintain their homes going forward. The difference between renovation success and disaster often comes down to this single planning decision—whether to embrace realistic preparation or succumb to the optimism bias that afflicts so many homeowners entering projects without adequate financial protection.

Start your renovation journey with eyes wide open to the reality that your home hides secrets even professionals cannot predict. Embrace contingency planning not as admission of doubt but as the hallmark of sophisticated project management. Your future self—living happily in a beautifully completed space without debt-related stress or quality compromises—will thank you for the wisdom to plan for the unexpected, even when optimism tempts you to do otherwise. The 20% rule isn't about preparing for failure; it's about ensuring success no matter what your home reveals during its transformation. In a world where nearly four out of five renovation projects exceed their budgets, the homeowners who plan for this reality aren't pessimists—they're realists who understand that proper preparation is the foundation of every successful renovation, transforming potential disasters into manageable challenges and turning renovation dreams into lasting reality that enhances both home value and quality of life for years to come.

DECEMBER 01, 2025

DECEMBER 01, 2025

DECEMBER 01, 2025

DECEMBER 01, 2025

NOVEMBER 28, 2025